Why Budgeting Fails Without Financial Literacy — and What to Do Instead

“Don’t tell me where your priorities are. Show me where you spend your money and I’ll tell you what they are.” — James W. Frick

Have you ever heard the saying, “money talks?” What we spend on tells a story about our goals, priorities, and biggest objectives. The real question is: are you listening to the narrative of your wallet?

Financial confidence is part of professional confidence.

According to the Certified Financial Planner Board, nearly 40% of Americans admit they’ve never created a personal budget at any point in their lives.1 Financially, this is like boarding a plane without knowing your destination. You might get somewhere, but it’s unlikely to be where you intended — and the journey will be far more stressful than it needs to be.

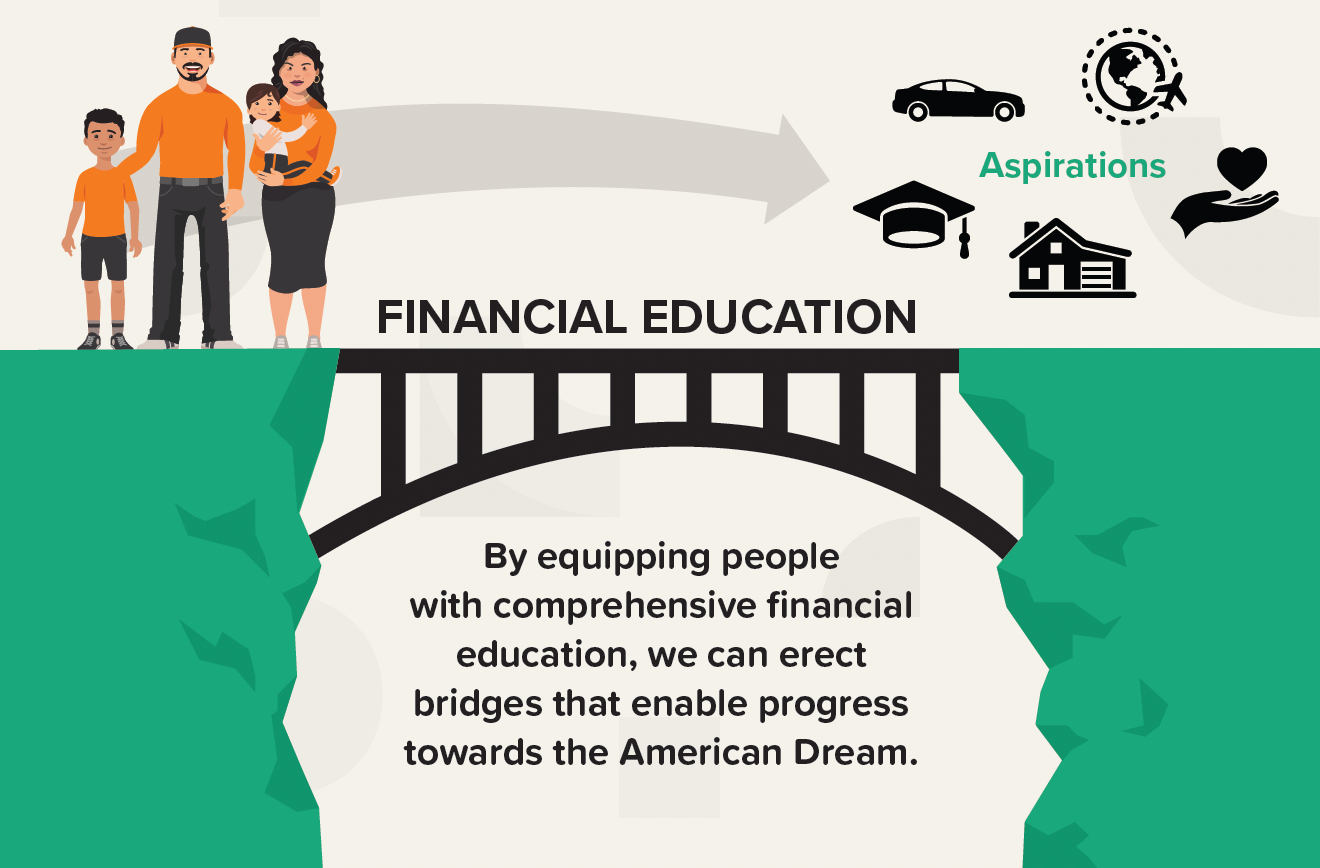

Many of us grew up with some notion of the “American Dream.” While it can mean different things to different people, it is generally the belief that if you work hard, attain the right education, and become skilled at something meaningful, you can shape a life that reflects your values and what you care about most. Maybe you want to travel to every continent, or perhaps you long for a furry companion that brings joy and anticipation. A recent survey of over a thousand adults found that these eight desires comprise the American dream for most people:

- Retiring in comfort (86%)

- Affording quality health care (86%)

- Owning a home (85%)

- Raising a family (78%)

- Owning a new car (72%)

- Going on vacation every year (71%)

- Caring for pets (66%)

- Having a wedding (55%)

These are wonderful ideas that nearly all people can agree should exist. But we must arm ourselves with the realization that it’s now been shown the American Dream costs over $5 million:

- Retirement: $1.6 million

- Owning a home: $957,594

- Owning a new car: $900,346

- Raising two children and paying for college: $876,092

- Health care: $414,208

- Annual vacations: $180,621

- Pets: $39,381

- Wedding: $38,200

Now, couple that with these unfortunate truths:

- One-third of American adults have nothing saved for retirement.

- Half of newlyweds go into debt to fund their wedding, with the average borrower saying “I do” with $11,737 of additional debt.

- 32% of students do not receive any financial assistance from their parents to pay for higher education, and the average college student graduates with almost $25,000 of student loan debt.

Is it such a surprise to learn that, perhaps most startlingly of all, the average individual with a bachelor’s degree earns about $4.21 million over their lifetime — far short of the $5 million price tag of the American Dream?

The truth is, knowing how to earn a living isn’t enough to make you financially literate. In addition to knowing how to earn and spend money, the Federal Reserve Bank of St. Louis defines financial literacy as understanding how to Grow, Manage and Invest your money, eventually turning it into an income stream that lasts beyond your working years.9 This skill is called financial literacy, and it equips you to reclaim control over your financial future. But to grow your money, you first have to save it. And how can you begin to save if you don’t know how much you’re spending? You don’t need to know calculus to understand that:

Savings = Earnings – Spending

You probably know your earnings well enough, but you cannot solve for “Savings” if you don’t know Spending. You cannot Grow your money without saving it. And if you are not Growing your funds, then you certainly cannot Manage what you do not have. (It goes without saying that you cannot Invest from nothing.) It becomes impossible to budget properly, therefore, without financial literacy.

Budgeting is an essential piece of financial literacy, and you cannot reach your destination without understanding how you drive, how you make decisions, and what motivates you to spend money on some occasions while being “stingy” on others. What causes are most important to you? What can you afford to reduce spending on without upending your daily living? How can you ensure that you won’t have to take a significant cut in your standard of living when you’re no longer earning an income?

Recommended Next Steps

1 . Analyze Your Cash Flow

List all your fixed monthly living expenses (rent, groceries, gas), then list all of your fixed optional expenses (subscriptions, entertainment, new clothing). Add these two values, then subtract the total from your monthly income. This difference is your discretionary income.

If this number is negative, you’ll need to decide what’s worth keeping, what’s nonnegotiable, and what can be modified or temporarily eliminated to prioritize financial planning.

2. Take the Financial Literacy Quiz

This short assessment provides a starting point for your financial journey and a personalized roadmap for next steps. You’ll receive a score across five pillars of financial literacy, highlighting strengths and areas for growth. Take the Quiz.

3. Use the 7 Money Milestones Framework

This step-by-step roadmap helps you stay on track without trying to perfect your entire financial life overnight. Begin with the basics — protecting income, establishing an emergency fund — then build toward long-term financial independence and security. Learn more.

In summary, budgeting is not about restricting your spending, but understanding your goals and having a plan to get there. It’s about awareness, intentionality, and control so you can align your spending with what’s important to you, bridge the gap between your dreams and reality, and eventually turn your money into a tool for freedom. Start budgeting today and unlock the full potential of your dollars, turning your efforts into a stream of experiences that money can’t buy.

Ready to take control of your money and your future?

Join The Lantern Network’s mentorship program and gain practical financial literacy skills through our Financial Literacy Workshop. Learn how to budget with purpose, plan with confidence, and make money work for your goals. Apply to become a mentee and start building a stronger financial foundation today.

Sources

- CFP Board, "No Matter Their Income or Assets, Need Support with Spending, Household Budgeting,” 2019.

- Investopedia, “The 2025 “American Dream” Now Costs More Than $5 Million,” 2025.

- USAToday, “The American dream now costs $5 million. Here's a breakdown,” 2025.

- Citizens Debt Relief, “1 in 3 Americans has saved $0 for retirement,”.

- LendEDU, “One-Third of Americans Go Into Unnecessary Debt to Pay For Extravagant Weddings—And Quite a Few End Up Regretting It,” 2019.

- Education Data Initiative, “How Do People Pay for College?” 2022.

- TheMoneyBooks, “HowMoneyWorks for the Next Generation,” 2025.

- Georgetown University Center on Education & The Workforce, "The College Payoff: Education, Occupations, Lifetime Earnings” 2009.

- Federal Reserve Bank of St. Louis, “What Is Financial Literacy and Why Should You Care?“ 2019.